The “official” story is that US tight oil operators have been holding steady since the outbreak of war in the Middle East. This is what publicly-traded operators have been saying on earnings calls. And indeed, if you look at the total frac crew counts in the top five oil basins (Anadarko, DJ, Eagle Ford, Permian and Williston), the trend looks flat at around 115 crews across the board.

Beneath the surface, however, the shale oil patch is splitting in two:

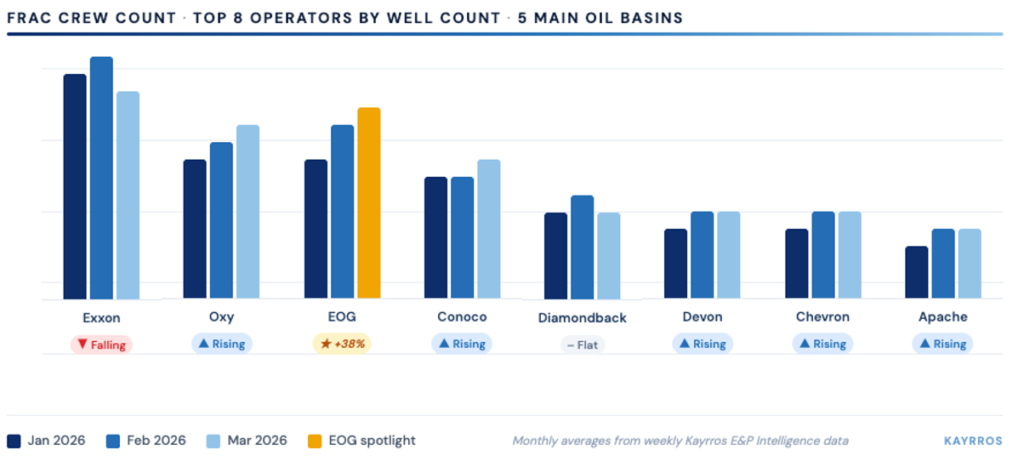

The Public Surge: Despite preaching “restraint” on earnings calls, public majors are stepping on the gas. Six out of the eight major operators are ramping up completions, with EOG alone adding three frac crews to its fleet in just six weeks. As a consequence, the Inventory of drilled but uncompleted wells have been reduced by roughly 12% as drilling activity continues its decline.

The Private Pullback: Private operators are not following the same steps. Even with WTI jumping $10 since the beginning of the conflict, their number of active frac crews has pulled back ~20% from its January peak and their active DUC inventory remains mostly flat year to date.

The “Earnings Gap”: There is a growing divergence between the rhetoric of last-quarter earnings calls and the physical ground-truth. Our geospatial data shows a completion race already underway.

The Bottom Line: On the surface, oil basin activity looks stable. In reality, two very different bets are being made on the future of energy. The unanswered question is, has the war triggered a bidding war for active frac crews in which major public companies have the upper-hand?

Interested in the full report or in learning more about our E&P Intelligence product? Get in touch here: https://www.kayrros.com/request-a-demo/