As talks – and speculation – about the potential reopening of the Strait of Hormuz gain momentum ahead of diplomatic meetings in Islamabad this weekend, much of the market commentary so far has focused on the number of laden tankers stranded in the Middle East Gulf. Another factor to consider in assessing how quickly normal crude supply from the Middle East Gulf can be brought back, however, is the amount of crude held at export terminals and readily available for loading. While crude inventories have risen significantly since the onset of the war, storage capacity at loading terminals is inherently limited, which has led producers to shut-in production early in the war, before running the risk of running out of storage capacity.

This report provides a notional estimate of crude stocks at Gulf terminals by country, in both absolute terms and days of incremental production needed to bring exports back to pre-war levels.

Executive Summary:

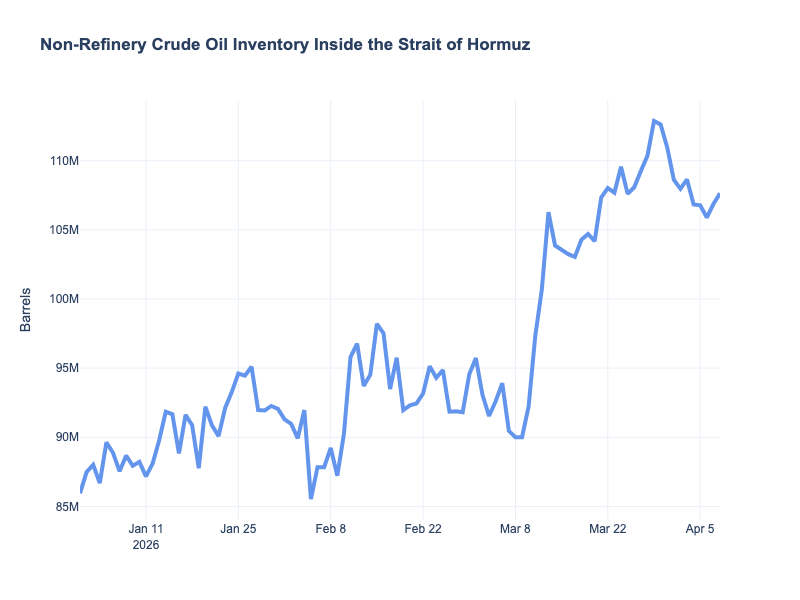

- In aggregate, Arab oil exporters in the Middle East Gulf hold an estimated 108MMb in onshore loading terminals along the Gulf coast. This excludes refinery and power station storage, as well as Saudi storage held on the Red Sea and UAE above-ground and underground stocks in Fujairah, which are not subject to the Hormuz blockade.

- Assuming total Arab Gulf output has been cut by 11.3 MMb/d since the onset of war, Arab Gulf onshore storage on paper covers nine and a half days of shut-in production, theoretically allowing exports to return to pre-war levels for that period of time without actually restoring production.

- If an additional 115 MMb in Arab Gulf floating storage is taken into account, exports could notionally reach pre-war levels for 20 days before production is restored.

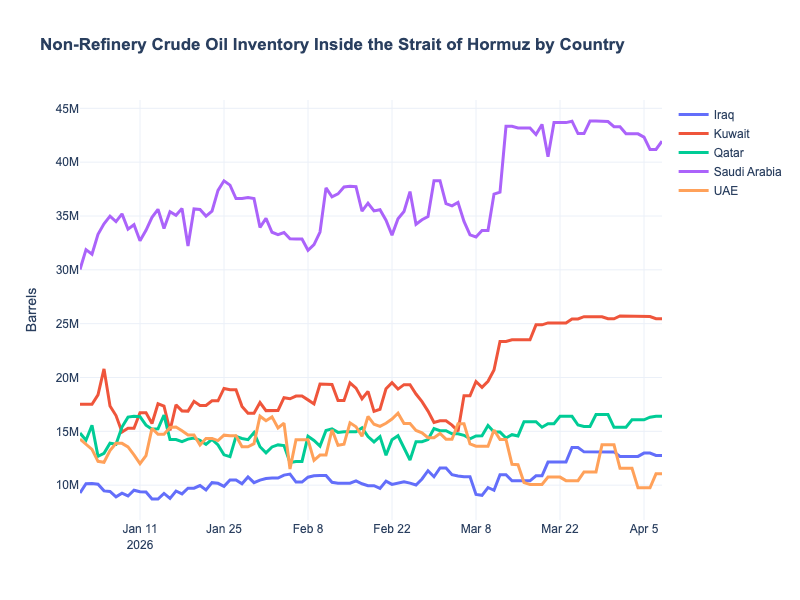

- Inventory levels vary greatly by country, both in absolute terms and in days of pre-war exports. Saudi Arabia, the Gulf’s largest producer and exporter, accounts for 40% of aggregate inventories, covering 10 days of shut-in Saudi production and exports. At one end of the spectrum, Qatar holds more than 16 MMb in crude and condensate inventories, or as much as 15 days worth of lost supply. At the other end, Iraq holds roughly 13 million barrels in storage, or just four days of shut-in supply.

- Even if Gulf traffic were deemed secure again and tankers immediately available to load, crude inventories (both onshore and offshore) are insufficient to make up for lost production before supply can return to pre-war levels. While there may be an initial flurry of exports as stranded tankers are allowed to depart and inventories are drawn down, this would run its course relatively quickly.

- The supply shortfall caused by the war will linger on for weeks if not months, even in a best-case scenario.

Crude stored at Gulf export terminals

- Despite production cuts, crude inventories on the Arab side of the Middle East Gulf built behind the Strait of Hormuz since the onset of the war. Crude stocks at oil export terminals are estimated at about 108 million barrels as of April 8. This excludes refinery and power station storage, as well as Saudi storage on the Red Sea and UAE underground and above-ground stocks in Fujairah, which are not subject to Strait of Hormuz restrictions. Crude stocks at Arab Gulf loading terminals shot up by 16% in the opening two weeks of the war, from February 28 to March 13, but builds subsequently slowed as Arab Gulf producers shut-in production to avoid running out of storage capacity and maintain stock levels below maximum operating levels (conventionally estimated at 80% of nominal capacity).

- In addition, at least 115 million barrels of crude oil is stranded on 72 tankers inside the Persian Gulf, Energy Aspects estimates. This only includes volumes on vessels with traceable AIS signals. It is unlikely that many “ghost ships” (with their transponders turned off) are stranded on the Arab side of the Gulf, however.

- In aggregate, nominal onshore crude stocks are sufficient to cover a maximum of nine and a half days of shut-in Arab Gulf crude supply (production and exports), or 20 days if floating storage is included. This estimate assumes lost Gulf crude and condensate production of about 11.5 MMb/d, as per Energy Aspects estimates. In practice, the actual volume of onshore stocks available for exports is likely significantly lower, as minimum operating levels (conventionally estimated at about 20% of nominal capacity) must be observed for storage tanks to maintain good operating standards.

Country-level crude stocks at Gulf export terminals

- Saudi Arabia, the region’s top producer and exporter, had an estimated 42 MMb of crude at export terminals inside the Persian Gulf. Assuming lost Saudi production and exports of 4.1 MMb/d due to the war, inventories cover roughly 10 days of lost crude supply.

- Kuwait has about 25.5 MMb in storage, or 11 ½ days of lost supply assuming production cuts of 2.2 MMb/d.

- UAE crude stocks at Gulf terminals amounted to an estimated 11MMb (not including Fujairah caverns and above-ground tanks) as of April 9, equivalent to just five and a half days of lost production (pegged at 2 MMb/d). The country has been able to partially bypass the Strait of Hormuz via its Habshan-Fujairah pipeline, avoiding large stock builds inside the Gulf.

- Iraq available stocks measured in days of exports are even lower, at an estimated 12 ¾ MMb, or just four days of lost supply.

- Qatar crude and condensate stocks were estimated at about 16MMb as of April 9, on the other hand, covering two weeks of lost supply (pegged at 1.1 MMb/d).

Note: The days-of-cover figures are rough estimates and are provided for indicative purposes only. Estimated losses in crude production are used as a proxy for export cuts for the purpose of this exercise. In practice. they may differ from actual cuts in export volumes. Some Gulf production capacity may have suffered lasting damage due to drone and missile attacks or uncontrolled emergency shut-in procedures. Thus, Saudi Arabia on April 9 stated that 600 kb/d of crude production capacity had been lost at Manifa and Khurais due to Iranian strikes, equally split between the two fields. The duration of production restarts will depend on a multiplicity of factors, including, but not limited to, the scope of field damage (if any) and how long it takes to procure spare parts, equipment, oilfield services and workers. Market participants willingness to ship through the Middle East Gulf may likewise depend on multiple factors, such as security arrangements and guarantees, costs and tanker availability.

In the news

- See us discuss this issue in the Financial Times (Financial Times)

- Devon Energy to Buy Coterra for $21.5 Billion to Create Shale Giant (WSJ)